What is the repeat offence rate and why is it an important parameter for fintech companies?

Fintech is booming. The number of apps and services in this industry is growing by the day. With new fintech companies emerging every day, it’s become increasingly important for them to understand the parameters that will make their company stand out from the rest.

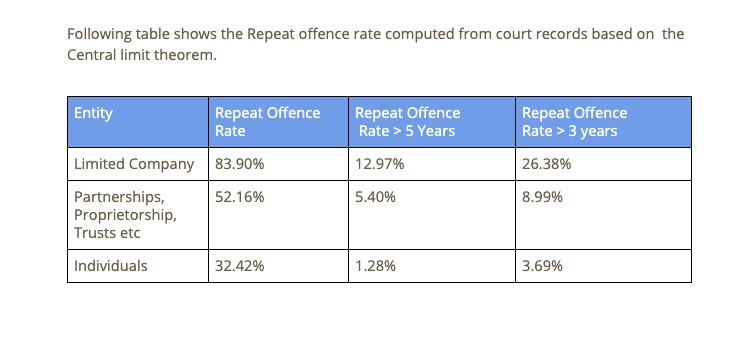

Repeat offence rate is a financial term that refers to the number of customers who commit more than one fraud over a period of time. It’s an important parameter for fintech companies because it helps determine how much money and resources will be spent on mitigating risk. If the repeat offence ratio is high, then the company can increase their spending on fraud prevention to make sure that customers are protected from fraud. This will help them avoid paying for fraudulent transactions by implementing anti-fraud software or engaging in identity verification processes like KYC (Know Your Customer).

What is a repeat offence? More importantly, who are repeat offenders?

People or organisations who have committed the same fraud or different more than one time are called repeat offenders. White-collar criminals are frequently characterised as “one-shot criminals” who do not re-offend after their first run-in with the law. Recent empirical research, on the other hand, contradicts this notion, demonstrating that white-collar criminals are frequently repeating offenders.

What does having a high repeat offence rate mean for fintech companies?

As India moves closer to becoming a cashless economy, the government has made a significant impact on the financial landscape, and online financial transactions are becoming familiar to millions of citizens. This has led to newer business models that generate both revenue and profitability.

Investment and fraud have a way of going hand in hand. This relationship has been further strengthened with the emergence of digital and retail currencies as they represent emerging opportunities for making quick money.

As per a report by ACI Worldwide which tracks and analyses real-time payment across 48 global markets, India ranked number one in real-time payments with 25.5 Billion transactions. The report points to the fact that fraud is increasing due to the fact that fraudsters target new channels. In India, 6.2% of fraud incidents occurred due to digital wallet account hacks. The most common types of digital frauds faced by companies consist of phishing/spoofing, identity fraud, account fraud and transaction fraud.

Fintech is one such industry where companies functioning within the sector cannot afford to go light on background checks. With rising financial crimes in the country, companies are more aware than before and are conducting verifications in a stringent manner. Nevertheless, fraudsters seem to be finding new ways to jump the hoops.

It’s no secret that there is a rise in the number of frauds committed against business organisations and individuals, many of which remain unresolved.

While there are several ways to evaluate the risk profile of a client, knowing their criminal background is one of the most important. Chances are if they have jumped the signal in the past, they will most likely do so in the future as well.

Fintechs usually steer clear of first-time offenders due to this.

How can fintech companies mitigate the risk of onboarding such clients?

Fraud prevention and detection is not a one-time activity. It’s a continuous process that requires continuous effort and coordination between various stakeholders. The key to prevention is to detect fraud at the stage of origination so that immediate action can be taken.

Today, data analysis is taken into account before a lending company decides to proceed with an account. The data on the transaction will be analysed and evaluated with multiple variables such as income, location, employment history and education are analysed from multiple data sources to understand the likelihood of a creditworthy transaction.

But that’s not quite enough.

Crime check is the way to go. Because even if the applicant bypasses the regular checks when a criminal check is done, and if they’ve portrayed criminal characteristics in the past, they’d definitely fall on the radar.

Criminal background verification is one of the most unavoidable formats of checks – it gives the organisation a thorough overview of the individual or company. From court records to FIR’s criminal background verification is an indicator of whether the person in question proves to be risky or not.

Fetching criminal records on individuals or companies once used to be the next to the impossible task in India. But with CrimeCheck, tables have turned. CrimeCheck is India’s leading online public court records & FIRs database. It covers all courts, police stations, and related forums across the entire country. With an exponential amount of data behind it, CrimeCheck has helped thousands of businesses make informed decisions with extensive background checks on their employees and clients.